INSURANCE SECTOR IN INDIA

2023 JUN 7

Mains >

Economic Development > Indian Economy and issues > Crop insurance

IN NEWS:

- Recently, the Insurance Regulatory and Development Authority of India (IRDAI) has allotted states and union territories to every insurer to increase insurance penetration in India and take insurance to every nook and corner of the country.

- This is in line with the IRDAI Vision 2047 plan, which aims at providing "insurance for all’ by 2047, the centenary year of India’s independence.

- The regulator is also planning to launch Bima Trinity—Bima Sugam, Bima Vistar, and Bima Vaahaks—collaborating with general and life insurance firms.

MORE ON NEWS:

- Through the framework called "Bima Trinity," IRDA is striving to create an "UPI-like moment" in the insurance sector.

- The following are three parts of the trinity envisaged by the IRDA:

- Bima Sugam:

- The Bima Sugam platform will integrate insurers and distributors on one platform to make it a one-stop shop for customers. Customers can pursue service requests and the settlement of claims through the same portal.

- Bima Vistar:

- Bima Vistar will be a composite insurance policy that covers life, health, property, and casualties or accidents, with defined benefits for each risk that can be paid out faster than usual without the need for surveyors.

- Bima Vaahaks:

- IRDA envisages a women-centric workforce of Bima Vaahaks (carriers) in each Gram Sabha that will meet the women heads of each household to convince them about the importance of a comprehensive insurance policy like Bima Vistar.

INSURANCE:

- Insurance is a contract, by which a company or the state undertakes to provide a guarantee of compensation for specified loss, damage, illness, or death in return for payment of a specified premium.

- There are mainly two types of insurances:

- Life insurance: It is a long-term insurance by which the insurance company pays an assured sum to a nominee in case of premature demise of the policy holder.

- General insurance: They are short-term insurances that cover non-life assets such as home, vehicle, health and travel.

HISTORY:

- 1818 saw the advent of life insurance business in India with the establishment of the Oriental Life Insurance Company in Calcutta. The colonial era was dominated by foreign insurance, like Albert Life Assurance and Royal Insurance.

- In 1956, the Government nationalized the Life Insurance sector and Life Insurance Corporation (LIC) came into existence. The LIC had monopoly till the late 1990s.

- Subsequently, the government nationalised the general insurance business in 1971.

- Following the LPG reforms in 1991, the insurance sector was open for private players.

- In 1993, R.N. Malhotra committee was set up to make recommendations for reforms in the insurance sector. The Committee recommended the inclusion of private players and foreign companies and creation of an Insurance Regulatory and Development Authority.

- In 1999, the Insurance Regulatory and Development Authority (IRDA) was constituted as an autonomous body to regulate and develop the insurance industry.

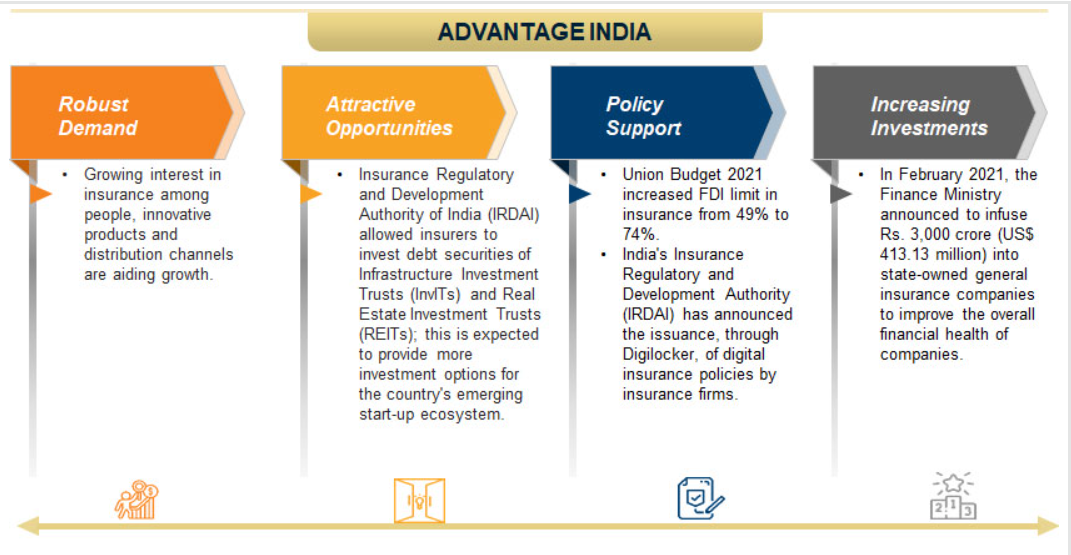

PRESENT STATUS:

- India is the 10th largest Life Insurance market and the 15th largest Non-Life Insurance market globally.

- Today there are 32 general insurance companies and 23 life insurance companies operating in the country. Together with banking services, insurance services add about 7% to the country’s GDP.

- Among the life insurers, Life Insurance Corporation (LIC) is the sole public sector company. There are six public sector insurers in the non-life insurance segment.

IMPORTANCE OF INSURANCE SECTOR:

- Provides safety and security:

- Insurance provides an ideal risk mitigation mechanism against events that can potentially cause financial distress to individuals and businesses.

- For instance, in case of business insurance, financial compensation is provided against financial loss due to fire, theft, mishaps etc.

- Spreads risk:

- The basic principle of insurance is to spread risk among a large number of people. A large population gets insurance policies and pay a small premium to the insurer. Whenever a loss occurs, it is compensated out of corpus of funds collected from the millions of policyholders.

- Encourages savings:

- Life insurance enables systematic savings due to payment of regular premium. The insured get the lump sum amount at the maturity of the contract.

- Promote financial inclusion:

- Insurance facilities, especially those supported by government, attract common man to utilise formal banking facilities.

- Eg: Crop insurance schemes like Fasal Bima Yojana have played an important role in promoting formal banking among Indian farmers.

- Generates long-term financial resources:

- Insurance sector generates funds by way of premiums from millions of policyholders. Due to the long-term nature of these funds, these are invested in government securities and stocks, which in turn funds long-term infrastructure assets such as roads and power plants.

- Strengthen financial stability:

- Insurers contribute to safeguarding of the stability of household and are among the largest investors in financial markets. Also, Government often relies on public insurance companies for stabilizing the economy, rescue ailing financial institutions or make investments in government undertakings.

- Eg: In August 2018, LIC was brought in by the government to rescue IDBI Bank Ltd.

- Promotes economic growth:

- By mobilizing domestic savings, insurance turns accumulated capital into productive investments, which in turn results in more employment and capital formation.

- Insurance also enables mitigation of losses, financial stability and promotes trade and commerce activities those results into sustainable economic growth and development.

CHALLENGES FACED BY THE SECTOR:

- Insurance gap:

- India’s insurance penetration (Insurance penetration defined as the ratio of total premium to GDP) was 4.2% in 2021, while insurance density (Insurance density is measured as a ratio of total premium to population) stood at USD 78 in FY20. This indicates that a large section of the population in India is uninsured.

- General insurance levels are still very low in India, which indicates that industries bear a significant proportion of risks while doing business in India.

- Government’s financial burden:

- While the government has been repeatedly infusing capital, the financial position of public sector general insurers continues to remain weak.

- Poor solvency ratio among public sector insurers:

- An insurer’s solvency is its financial capacity to meet its obligations. The solvency ratio (size of an insurer’s capital in relation to the risk) of the public sector general insurance companies is lower than the regulatory minimum of 1.5, which affects the ability of insurance firms to settle claims.

- Lack of financial literacy:

- According to a recent survey by the Securities and Exchange Board of India, only 27 per cent of India's population is financially literate. This hinders the penetration of insurance into common man’s life.

- Issues with accessibility:

- Even though insurance players have opened Tier II and III branches in cities, their rural participation remains deficient.

- Despite digitisation, insurance products are mostly offered and marketed in traditional ways that make it tougher for advanced insurance plans to gain traction.

- Fear of premium hike and claim rejection:

- As a result of the ongoing consolidation and privatisation of insurers, there is a likelihood that premiums and claim rejection will increase. Both these developments will have a chilling effect on the customers.

- Vulnerability to global financial variations:

- With more foreign private entities in the Indian market, the sector will be more exposed to the global markets. This means that in case of a global economic crisis like the one in 2008, the insurance sector could be severely affected.

WAY FORWARD:

- Promote awareness:

- There is a need to promote awareness on financial literacy and importance of insurance among the common man.

- Increase accessibility:

- Introducing and implementing new channels of distribution is essential to improve rates of penetration and density, especially in rural areas. Hence, facilities like bancassurance must be encouraged.

- Diversify choice:

- The Covid pandemic has made people realise the importance of having adequate health coverage. Hence, a greater number of insurers and low-cost insurance products are essential for Indian customers.

- Encourage privatisation:

- The insurance sector in the country is growing at a speedy rate of 15-20%. Increasing private participation would help enhance accelerate this trend.

- Revitalise existing insurers:

- While pushing ahead with privatisation, there should also be efforts to address issues such as vacancies within the present system.

- Develop capital market:

- To facilitate the entry of new players, the capital market, particularly the secondary market needs to be enlarged.

- Strengthen regulator:

- The IRDAI needs to be equipped to exercise its vigilance on matters concerning premium rates, claim settlement, regulation of unfair practices etc.

- Encourage financial literacy:

- People, especially those in the informal sector, must be made aware of the benefits of insurance and encouraged to avail them.

PRACTICE QUESTION:

Q. Insurance sector is an important element in the operation of national economies throughout the world today. In this regard, analyse the prospects and challenges of insurance sector in India?