Mains >

Economic Development > Indian Economy and issues > Cooperatives

Syllabus

GS 3 > Indian Economy > Banking sector

REFERENCE NEWS

The recent Karuvannur Cooperative Bank scam has again brought to the fore the governance issues in the functioning of Cooperative Banks in India. PMC Bank, Guru Raghavendra Cooperative Bank and Maharashtra State Cooperative (MSC) Bank have also failed in recent times.

ABOUT COOPERATIVE BANKS

Cooperative banks in India are financial institutions that operate on a cooperative basis, where the customers are also the owners of the bank.

Cooperative banks operate on the principle of ‘no profit, no loss ‘and ‘one person, one vote ‘.

According to the Reserve Bank of India (RBI), India had 1,502 urban co-operative banks as of March 2023.

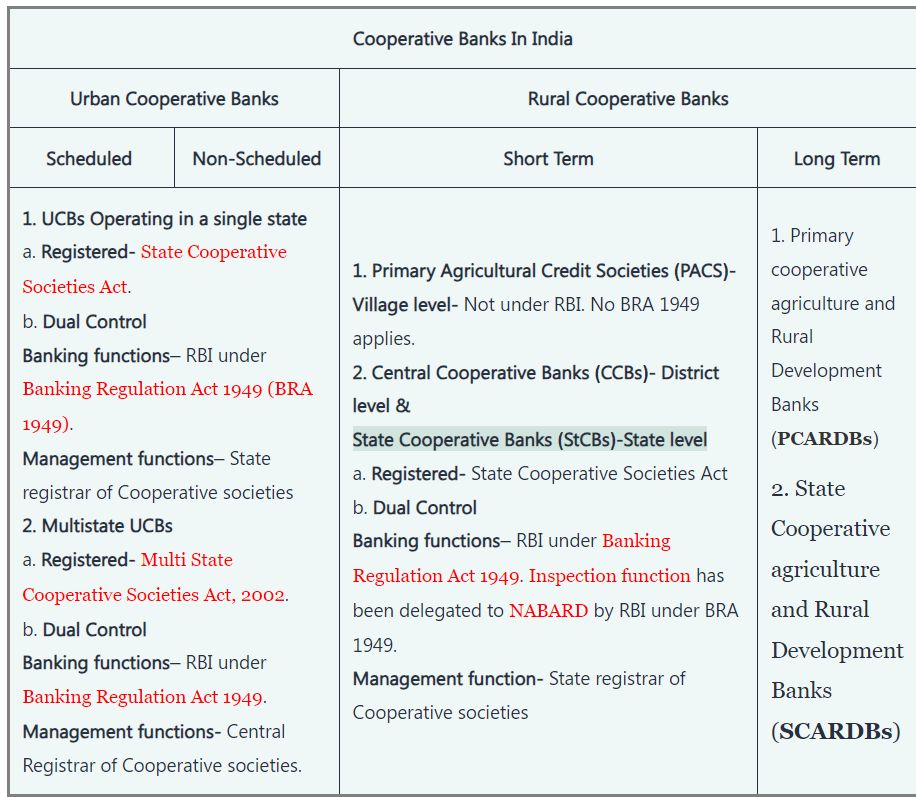

STRUCTURE OF COOPERATIVE BANKS IN INDIA

IMPORTANCE OF COOPEARTIVE BANKS

Agricultural and Rural Development: Cooperative banks are instrumental in bolstering the agricultural sector. They extend essential credit facilities to farmers, aiding in crop production, equipment purchase, and other agricultural activities. This support is vital for rural development and food security. Ex: In regions like Punjab and Haryana, these banks have significantly contributed to the Green Revolution, enhancing agricultural productivity and rural income

Supporting Local Businesses and Self-Help Groups: Urban Cooperative Banks (UCBs) provide critical financial services to Micro, Small, and Medium Enterprises (MSMEs) and Self-Help Groups (SHGs). This support helps in fostering local entrepreneurship and employment. Ex: Funding of Lijjat Papad, a women's cooperative, which showcases how cooperative banks can empower small-scale industries and women-led enterprises.

Democratic Governance: Cooperative banks are owned and managed by their members, who democratically elect their board of directors. This structure ensures that the bank's policies and decisions are aligned with the interests of its members. Ex: In regions like Maharashtra, Kerala, and Gujarat, where cooperative movements are strong, this has led to greater political empowerment and community involvement in financial decision-making.

Member-Focused Services: Unlike commercial banks, cooperative banks prioritize serving their members' needs over profit maximization. They offer personalized financial products, such as tailored savings schemes and affordable housing loans, to meet the specific requirements of their members. This approach not only benefits individual members but also strengthens the overall financial health of the community.

Community Empowerment and Development: Cooperative banks play a pivotal role in community development by funding local infrastructure, educational initiatives, and healthcare projects. Ex: In regions like Sikkim, cooperative banks have been instrumental in financing local development projects, thereby enhancing the region's socio-economic growth.

Economic Resilience: Cooperative banks tend to be more resilient during economic downturns, as their exposure to high-risk and high-value assets is generally lower compared to commercial banks. This was evident during the Global Financial Crisis of 2008, where many cooperative banks, particularly Urban Cooperative Banks (UCBs), demonstrated notable stability compared to their commercial counterparts.

Promoting Financial Inclusion: Cooperative banks play a significant role in promoting financial inclusion, especially in underserved and rural areas where access to traditional banking services is limited. They offer basic banking services, such as savings accounts and small loans, to individuals who might otherwise be excluded from the formal banking system.

Catalyst for Social Change: Beyond financial services, cooperative banks often initiate and support various social causes, such as literacy programs, women's empowerment, and environmental sustainability initiatives. By aligning their operations with broader social goals, they contribute to the overall welfare and progress of the communities they serve.

ISSUES WITH COOPERATIVE BANKS

Incidence of Financial Scams: A major challenge for cooperative banks in India is their vulnerability to financial scams. Notable examples include the failures of PMC Bank, Guru Raghavendra Cooperative Bank, and Maharashtra State Cooperative (MSC) Bank, which were attributed to financial frauds. These incidents undermine public trust and threaten the stability of the cooperative banking sector.

Conflict of Interest with Board Members: Unlike commercial banks, cooperative bank board members are allowed to borrow from their banks. This privilege has been misused in several instances, leading to significant financial losses. The PMC Bank scandal is a case in point, where the misuse of borrowing powers by board members played a role in the bank's failure.

Political Influence and Corruption: The governance of cooperative banks often falls under the influence of local politicians. This political entanglement can lead to malpractices like issuing unauthorized loans and facilitating illicit financial transactions, thus compromising the banks' integrity and financial health.

Financial Instability: Cooperative banks frequently grapple with issues like inadequate capitalization, high levels of Non-Performing Assets (NPAs), and low Capital Adequacy Ratios (CAR). These financial vulnerabilities limit their ability to operate effectively and expand their services.

Competition from New Financial Entities: The growth of Microfinance Institutions (MFIs), FinTech companies, payment gateways, and Non-Banking Financial Companies (NBFCs) has introduced significant competition. This has impacted cooperative banks' deposit and lending capabilities, as these new entities often offer more modern and accessible financial services.

Regulatory Ambiguities: Cooperative banks in India are subject to dual regulation – by the Reserve Bank of India (RBI) for banking functions and by state governments for administrative operations. This dual control creates regulatory complexities and sometimes leads to ineffective monitoring and governance.

Inadequate Audit Practices: The audit mechanisms employed by state departments are often irregular and lack thoroughness. This insufficiency in auditing contributes to the risk of financial mismanagement and fraud within cooperative banks.

Infrastructural Limitations: Many cooperative banks struggle with outdated infrastructure, such as subpar software systems and inadequate bookkeeping practices. These limitations make them more susceptible to operational inefficiencies and fraudulent activities.

Governance Difficulties: The small size and dispersed nature of cooperative banks, coupled with the absence of a unified brand or policy framework, pose significant governance challenges. This fragmented structure makes effective oversight and uniform policy implementation difficult.

Technological Lag: Compared to commercial banks, many cooperative banks lag in adopting advanced technology. This technological gap affects their operational efficiency, customer service, and ability to compete in an increasingly digital banking landscape.

Limited Geographic Reach and Scope: Most cooperative banks have a limited geographic presence and scope of services. This constraint hampers their ability to scale up and diversify their offerings, limiting their competitiveness and growth potential.

WAY FORWARD

Strict Regulatory Action by RBI- RBI must be stringent in its regulatory oversight by focussing on regular delicensing and the shrinkage or compulsory amalgamation of loss making cooperative banks.

Cooperative Federation- A cooperative federation must be formed to conduct regular comprehensive audits of the cooperative banks.

Upgradation of infrastructure- The provisions must be made for a common, standardized software, standardized bookkeeping systems. These must be linked to a central database for proper financial monitoring using artificial intelligence and pattern recognition.

Remove political influence- There is a need to bring in new people, young people and professionals in managerial roles, who will take cooperative banks forward.

Implement the recommendations of N.S. Vishwanathan Committee- Four tier classification (Tier 1 (having deposits up to Rs 100 crore), Tier 2 (deposits between Rs 100 crore and Rs 1,000 crore), Tier 3 (deposits between Rs 1,000 crore and Rs 10,000 crore), Tier 4 (deposits more than Rs 10,000 crore)), formation of board-level Committees, constitution of professional board of management and fixed tenure of board members recommended by the committee must be implemented at the earliest.

Implement recommendation of R Gandhi Committee- Conversion of Urban Cooperative Banks (UCBs) with business size of 20,000 crore rupees or more into regular banks.

Hence, the path forward for India's cooperative banks lies in balancing their community-centric role with strengthened governance and modernization, ensuring their resilience and relevance in the evolving financial landscape.

PRACTICE QUESTION

Q: How are cooperative banks different from Scheduled Commercial Banks? Examine the advantages, challenges of cooperative banks, along with suggestions for their better performance. (15M, 250W)