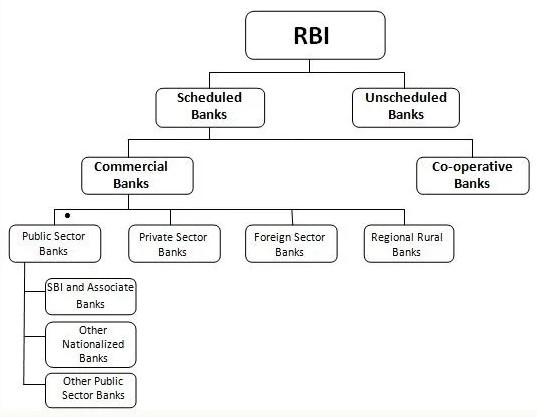

Regional Rural Banks (RRBs)

2022 AUG 3

Preliminary >

Economic Development > Indian Economy and Issues > Banking sector

Why in news?

- Government has recently reviewed the financial and operational reforms for RRBs.

More about news:

- Reform is aimed at making RRBs financially sustainable, more digitized and increasing their credit base especially to MSME sectors (for increased profitability)

- RRBs Provide banking to rural masses, support weaker sections (through credits), direct finance to cooperative societies and SHGs, reduce regional imbalances and increase rural employment generation.

- Most of the RRBs are in loss, poor management practices, NPA is increasing and lacks unity of command (being controlled by govt. as well as sponsor banks such as NABARD, RBI)

About Regional Rural Banks (RRBs):

- It was formed under RRB Act 1976 (recommended by Narasimha Working Group (1975)), for providing credit in rural areas.

- Ownership:

- Central Government (50%)

- Concerned State Govt. (15%)

- Sponsor Bank (35%)

- It was to follow priority sector lending (75%) on the same level as commercial Bank

- The first Regional Rural Bank “Prathama Grameen Bank” was set up on 2nd October 1975.

- The RRBs combine the characteristics of a cooperative in terms of the familiarity with the rural problems and a commercial bank in terms of its professionalism and ability to mobilise financial resources.

- RRBs are to maintain CRAR (Capital-to risk-weighted asset ratio) of a minimum of 9% (at par with commercial banks)

- CRAR is the ratio of a bank’s capital in relation to its risk-weighted assets and current liabilities.???????

PRACTICE QUESTION:

Consider the following statements regarding ‘Regional Rural Banks (RRBs)’

1. They are scheduled commercial banks operating under RBI

2. They have to maintain CRAR (Capital-to Risk-Weighted Asset Ratio) as prescribed by RBI

Which of the statements given above is/are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Answer